While auto shows have generally started to lose some significance as automakers turn to dedicated launch events, this year's Shanghai auto show could be an exception, said Deutsche Bank analyst Edison Yu's team.

(A file photo taken by CnEVPost at the Shanghai auto show two years ago shows an ET7 wrapped in a blanket.)

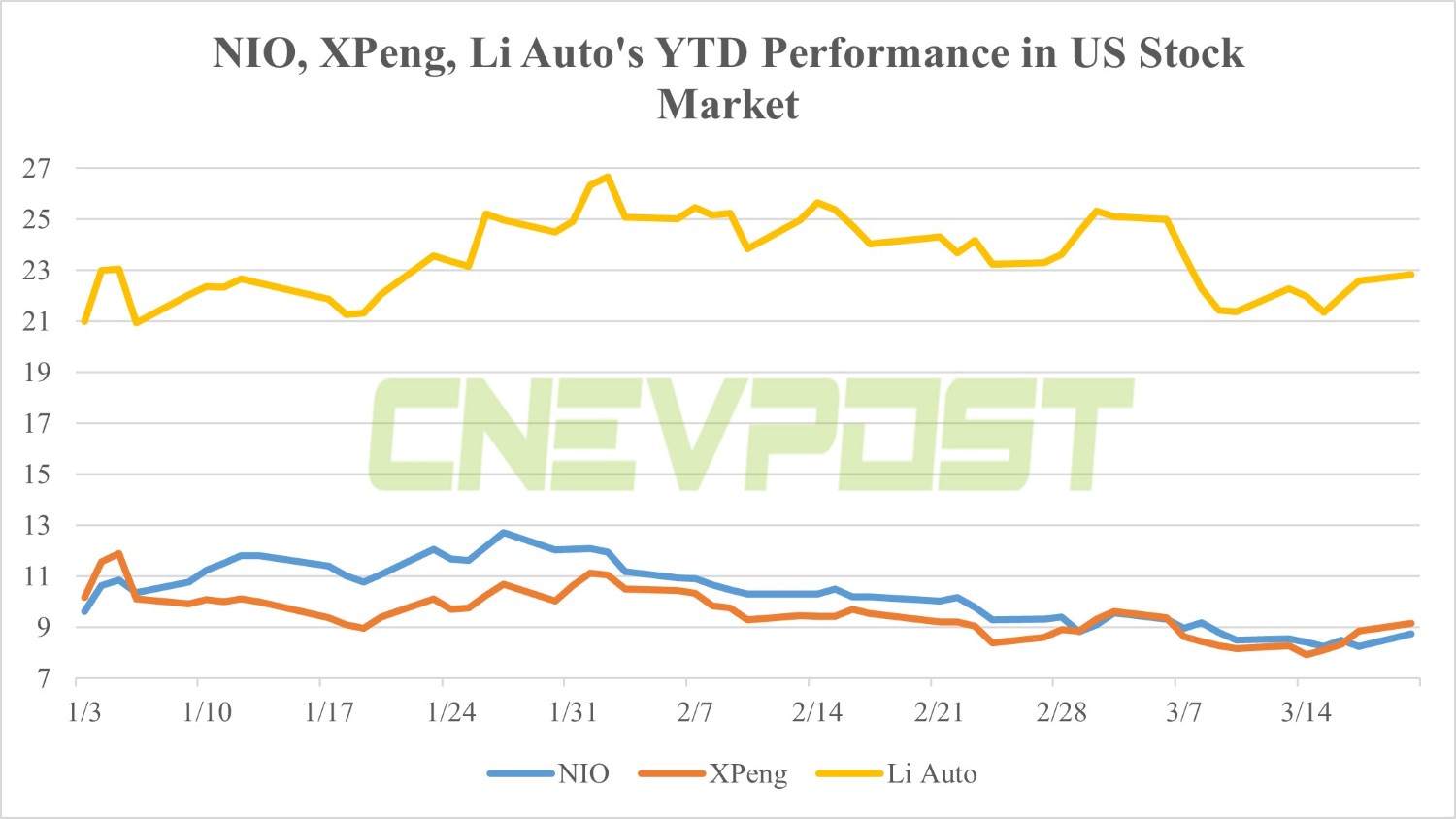

The Shanghai auto show will begin in less than 10 hours, and it will be interesting to know what analysts expect from the event.

"While auto shows have generally started to lose some significance as OEMs shifted to dedicated launch events, this year's Shanghai Auto Show (starts officially tomorrow) could be an exception," Deutsche Bank analyst Edison Yu's team said in a research note sent to investors today.

Most notably, this will be the first auto show since Covid reopened, bringing together many executives and industry observers from overseas for the first time in years, the team said.

Product cycles for electric vehicles are significantly faster compared to internal combustion engine vehicles, as automakers struggle to maintain customer attention and loyalty, meaning many of the vehicles unveiled at the show will begin delivery in short order, the team noted.

NIO (NYSE: NIO), XPeng (NYSE: XPEV) and Li Auto (NASDAQ: LI) all have new announcements coming this week, with NIO set to officially unveil its new ES6, historically its best-selling SUV, Yu's team wrote.

NIO's sales have been sluggish in recent months due to customer expectations of a platform changeover, so the new ES6 will be a very important product, with deliveries likely to begin in June, the team said.

In addition to the new ES6, NIO will also unveil the new ET7 at the Shanghai auto show, the flagship sedan whose sales in the past few months have been well below its performance in the second half of last year.

The updated version of the NIO ET7 will feature some improvements to its interior and deliveries are expected to begin in a few months, Yu's team said.

For XPeng, it will unveil its G6 SUV at the show, which Yu's team believes is the most important model for the company's ambition to reignite volume growth.

"Pricing details will likely not be finalized though as management gauges the initial consumer response. Deliveries are set to begin in June," the team wrote.

Li Auto will launch its dual-energy strategy by unveiling its all-electric solution tomorrow.

The company's first BEV will be a premium MPV and production is expected to begin by the end of this year, Yu's team noted.

Li Auto management recently said it plans to spend RMB 10 billion yuan to build 3,000 supercharging stations by 2025, and further details of this roadmap are to be expected, the team said.

In addition to these three Chinese upstarts, traditional Chinese OEMs have been very active over the past year, the team said.

So far, GAC and Zeekr have been the most consistent in terms of volume, according to the team.

Zeekr plans to bring the recently launched Zeekr X compact SUV to Europe along with the Zeekr 001 shooting brake model, and more details on the European strategy will be provided this week.

Also, BYD has been quite active, showing off its new Yangwang U9 electric supercar with the new DiSus-X body control system last week.

This week, BYD will unveil the Song L BEV and also begin taking pre-orders for the U8, a premium off-road SUV.

" The company is clearly trying to move upmarket by establishing bold 'halo' vehicles for its new brand," Yu's team wrote.

BYD also announced that the Dolphin and Seal BEVs will be available in Europe later this year. Both models will be smaller and cheaper and should compete more effectively in the low end of mass market, the team said.

In addition to local Chinese carmakers, global OEMs are also showing off new products, and upcoming new models will include the Polestar 4, Smart #3, Lexus LM and Maybach SUV BEV, the team noted.

Shanghai auto show: Full schedule of 150 press conferences for exhibitors

The post Shanghai auto show: Deutsche Bank's preview appeared first on CnEVPost.

For more articles, please visit CnEVPost.

The team calls NIO management's long-term strategy the Blue Sky Blueprint, saying it will be a moat for the EV maker, though it's very costly to build.

The team calls NIO management's long-term strategy the Blue Sky Blueprint, saying it will be a moat for the EV maker, though it's very costly to build. "Even if we exclude these one-time headwinds, vehicle of margin of 13.5% would have been a miss and lowest since 2Q20," Deutsche Bank said.

"Even if we exclude these one-time headwinds, vehicle of margin of 13.5% would have been a miss and lowest since 2Q20," Deutsche Bank said. Fitch expects sales of passenger NEVs in China to grow by more than 30 percent in 2023, while ICE vehicles will decline by the low teens.

Fitch expects sales of passenger NEVs in China to grow by more than 30 percent in 2023, while ICE vehicles will decline by the low teens. Deutsche Bank expects the latest round of price cuts to spur a big rebound in EV orders, with at least eight automakers already offering some type of price discount or promotion so far.

Deutsche Bank expects the latest round of price cuts to spur a big rebound in EV orders, with at least eight automakers already offering some type of price discount or promotion so far. CICC expects the first quarter to contribute 15.7 percent of China's 2023 NEV sales, with 20.7 percent, 27.6 percent and 35.9 percent from the second to fourth quarters, respectively.

CICC expects the first quarter to contribute 15.7 percent of China's 2023 NEV sales, with 20.7 percent, 27.6 percent and 35.9 percent from the second to fourth quarters, respectively.