XPeng announced its fourth-quarter earnings today and held a conference call with analysts.

Below are the key points mentioned by XPeng chairman and CEO, He Xiaopeng, during the call.

Inflection point

XPeng is approaching an inflection point, as we have clearly identified what our goals are, and what our strengths and weaknesses are.

Our overarching goal is to make XPeng a leader in the Chinese EV market, and ultimately win the global EV race.

Senior hire & org changes

The organizational restructure started with changes and upgrades in our top leadership. Ms. Fengying Wang brought us more than 30 years' experience in the automotive industry.

Fengying is taking full responsibility for our product planning and sales operations, and is also in charge of our product platform management scheme.

Her extensive industry experience, in-depth market insight and strong execution capabilities will help our products capture customer demand more accurately, while greatly improving efficiency in our sales and services divisions.

At the same time, the adaptations to our managements' organization are geared toward a flatter and more concentrated structure.

Since February, all design, R&D, production, supply chain and organizational management functions directly report to me.

I believe that these shifts will significantly improve our planning capabilities and lift the efficiency of our decision-making and execution in the coming months.

More importantly, these adjustments have effectively refreshed our execution and competitiveness. For the foreseeable future, I will remain focused on lifting the labor efficiency across our organization by multiple times so as to generate increased customer value with the same headcount, and greatly reduce costs across a full range of processes through technology innovation.

Product planning and design

With regard to our product planning and design, we concentrate on customer-perceived value and product differentiation in our innovation. We will make substantial changes to future products' model configuration mix, whole-vehicle modularized design and consistency in smart features.

In terms of interior and exterior styling and design, to meet XPeng customers' high standards for aesthetics, I am directly running the styling design division and building three teams that compete with each other to generate creative ideas.

These initiatives will continuously improve our interior and exterior styling and space design capabilities.

Customer-centric

We incorporated the Net Promoter Score, or NPS, into the core performance indicators for a variety of business functions and require feedback collection on a monthly basis.

The NPS performance evaluation will anchor the transformation of our product planning, design and development toward a customer-centric pathway. I believe our new products, new OTAs and new services-to-come will demonstrate substantial progress.

New P7i launch

Our in-store traffic and test-driving volume both hit new heights in recent months following the P7i's launch. This new product's smart features, styling design and performance, among other clear advantages in rivalry with similar products were well received among customers.

Amid the market's prevailing weakness in new order intake, our results outperformed the market. Our new order intake in February increased 100% over the previous month.

With the strong momentum of P7i orders following its official launch, we expect to see a considerable month-on-month growth of total new order intake in our March. This marks an initial success following our comprehensive transformation, which has also boosted our company morale.

New SUV G6

Our second new product model coming up this year – the G6 – will make its debut at the Shanghai auto show. Its official launch and vehicle deliveries will occur around the middle of this year.

The G6 will bring the most advanced electrification and smart mobility technologies to the 200,000 to 300,000 yuan-priced NEV SUV market. With unrivaled interior space, range, styling and interior decoration, we believe the G6 will become the top-selling model in its market segment.

Following the ramp-up of G6's mass production, we expect G6's monthly sales target to be 2 to 3 times that of its P7 predecessor's sales.

In addition, in the second half of 2023, we will launch a brand-new BEV 7-seat MPV.

This new MPV model is designed to cater to customer cohorts that demand larger interior room, while serving the needs of our family customers for a human-machine co-pilot.

Chat GPT

Recently, Chat GPT4.0 and other AI-based applications have created a buzz among hundreds of millions of users on the massive potential of generative AI models.

Given this development, there is an even higher possibility that autonomy technology further advances from Level 4 to Level 5.

We expect to incorporate GPT technology deeply into XPeng's business across the board to create groundbreaking user experiences and exceptional improvements to our operational efficiency.

XNGP

In March, we began to accelerate the OTA rollout of City NGP, compatible with multiple models, in several cities including Guangzhou, Shenzhen and Shanghai.

Through City NGP's OTA, we took the lead in mass producing the Transformer-based BEV time-series network, XNET, in China, which achieved a milestone in deep learning algorithm development and application.

In the second half of this year, XNGP, powered by XNET's deep learning algorithms, will no longer depend on a high-definition map. That said, XNGP will be supporting drivers on more urban roads, and across even broader geographic coverage nationwide.

Results from our testing showed the new version of XNGP outperformed peer's actual on-road performance in the United States. This leads us to believe XPeng's autonomous technology and its customer adoption is approaching a pivotal turning point.

While keeping high safety standards remains a top priority of our technology advancements, we will also be focused on rapid development to improve scenario coverage, user experience and software and hardware cost optimization.

In terms of scenario coverage, we have expanded the usage of the advanced technology from highway scenarios into city scenarios, where ADASs are used at high frequency and even become an essential driving tool.

Going forward, we will strive to further broaden ADAS usage to more end-to-end driving scenarios, such as internal compound ways and non-public roads, and expand our geographic coverage from three cities to more major cities nationwide beginning in the third quarter.

In terms of user experience, we have achieved an important psychological barrier for customers to use autonomous driving to "relieve" drivers, that is, drivers can let the machine safely take the wheel, resting assured that they are acting only as a supervisor.

Looking ahead, we expect that through continuous OTA upgrades, XNGP's driving skills will escalate every year and in 2-3 years reach a level that is equivalent to a human driver with 3 years of driving experience. We also expect that the number of manual takeovers per 100 km will be reduced to one or fewer.

Cost cut

Regarding cost efficiency, we plan to cut XNGP's BOM cost significantly next year and adjust our sales model from one that bundles sales of software and hardware, to one that splits the sales of software and hardware, which is going to enable autonomous driving on all of our new vehicles, and allow more customers to use the latest autonomous driving capabilities.

In pursuit of breakthroughs in the aforementioned three realms, we will bring great value to our customers and build out competitive edge in technologies, delivering long-term, sustainable revenue growth at scale and with improved margin contribution.

It has been said that the past five-year period was the golden age for new energy vehicles. I believe the next five-year period will be the golden age for autonomous driving.

During the five years to come, XPeng's highly advanced autonomous driving technology will help XPeng accelerate our ability to gain top market share.

More powerful cost control will be the core competitive edge that will enable XPeng to secure its leadership in the EV market. We will advance the platform-based approach and technology innovation to propel our cost reduction strategy.

Platform approach

Entering 2023, we are applying a full platform engineering approach for our BEV vehicle platform, electrical and electronic architecture, powertrain system and ADAS software and hardware development.

This signals that we are entering a new phase of car-making in a unified system. In this way, we are able to develop products with superior customer experience at a faster pace and a lower cost.

In the past, our R&D strengths were primarily manifested by our leading product performance. In the future, our R&D strengths will be underlined by maintaining the leading performance while achieving remarkable cost reductions.

We have mapped out our strategic execution roadmap with associated cost reductions include an over 50% decrease for autonomous driving costs and an about 25% decrease for vehicle hardware costs (including powertrain) over the 2023-2024 period by means such as technology innovation and optimized configurations.

I am pleased to see the design, technology R&D, supply chain and manufacturing teams are now working in a synergetic way to make our products more competitive through innovation.

Cash resources

In terms of cash liquidity, our cash on hand at the end of 2022 amounted to over RMB38 billion. As we have nearly completed our investments in our two manufacturing bases over the past few years, our Capex will decline substantially. We have also established three powerful vehicle platforms that can support a serial of new model launches over the next three years.

Our R&D will further concentrate on initiatives that best correspond with long-term trends and further differentiate our product in terms of customer experience and cost. We will also pursue improvements in our operating efficiency throughout the entire process.

For example, within our sales operations, we strive to improve same-store efficiency by optimizing our store network. We believe these cost optimization efforts will start to deliver material results beginning in the second half of this year.

Expanding scale

Expanding our scale and market share to achieve economy of scale in both software and hardware is the primary goal in our long-term strategy.

Although the product and management adjustment cycle in the automotive industry is more difficult than other industries and takes a longer period of time, we are still willing to sacrifice short-term sales and more patiently pursue greater victories in the medium- and long-term.

Looking ahead

Excitingly, as we rapidly implement adjustments and changes to our management, in addition to instituting a host of upgrades and iterations in our product portfolio and marketing capabilities, we have seen encouraging changes and positive results.

I am firmly convinced that beginning in the third quarter of this year, XPeng's monthly sales number will achieve significant growth, both sequentially and year-over-year, as well as be much higher than the industry's average growth rate.

I would reiterate that our current focus is on building and improving our capabilities in organization, product design, marketing and cost control. Continuous efforts in refining management and accelerated new product launches in the era of autonomous driving will lead us to the next level of exponential growth. We will continue to strive for this goal.

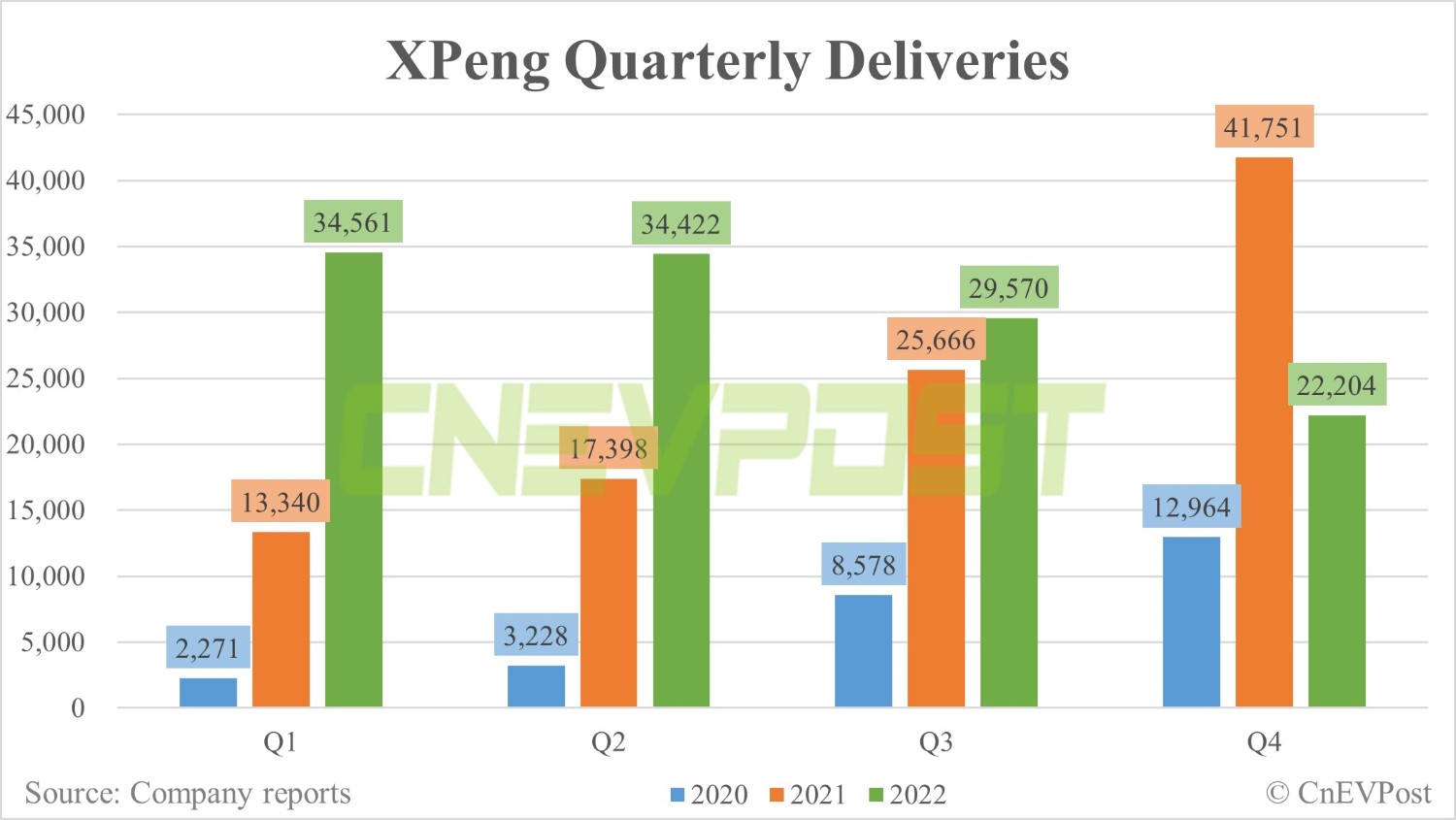

Lastly, we expect our total vehicle deliveries to be between 18,000 and 19,000 units in the first quarter of 2023 and revenue to be between RMB4 and RMB4.2 billion.

XPeng Q4 revenue misses estimates, gross margin falls to single digit

The post XPeng Q4 earnings call: Key points of transcript appeared first on CnEVPost.

For more articles, please visit CnEVPost.